Introduction to Neural Networks

From Linear Regression to Deep Networks

Noel Jeffrey Pinton

Department of Computer Science

University of the Philippines Cebu

Neural Networks

What We'll Cover

Linear Regression

Predicting continuous values

Gradient Descent

Optimizing parameters

Logistic Regression

Binary classification

Regularization

Preventing overfitting

History of NNs

80 years of progress

Simple Neuron

The perceptron

Multilayer Perceptron

Hidden layers

Fully Connected NNs

Deep networks

Learning Objectives

Regression

Explain linear and logistic regression, compute predictions by hand, and understand residuals & cost functions

Gradient Descent

Derive the MSE gradient step-by-step using chain rule, and apply gradient descent to optimize parameters

Regularization

Describe overfitting vs. underfitting and explain how L1, L2, and dropout prevent memorization

History

Trace 80 years of neural network development from McCulloch-Pitts to ChatGPT

Neurons & Logic

Compute forward passes through perceptrons and build AND, OR, NOT gates from single neurons

Deep Networks

Explain how hidden layers solve XOR, work through backpropagation by hand, and count FCNN parameters

Linear Regression

What is Linear Regression?

Definition

A supervised learning method that models the linear relationship between a dependent variable \(y\) and one or more independent variables \(x\).

$$\hat{y} = w_0 + w_1 x_1 + w_2 x_2 + \ldots + w_n x_n$$

Or in vector form: \(\hat{y} = \mathbf{w}^T \mathbf{x} + b\)

Goal

Find the "best fit" line that minimizes the distance between predicted and actual values.

Why Linear? A Real-Life Analogy

Your electricity bill

Monthly charge = base fee + rate per kWh × usage

\(\text{Bill} = 500 + 12 \times \text{kWh used}\)

The connection

This is exactly \(\hat{y} = w_0 + w_1 x\) where:

- \(w_0 = 500\) (base fee / intercept)

- \(w_1 = 12\) (rate / slope)

- \(x\) = kWh used (input feature)

- \(\hat{y}\) = bill amount (prediction)

Many things are "roughly linear"

- Distance traveled = speed × time

- Taxi fare = base + rate × km

- Exam score ≈ hours studied × factor

- Crop yield ≈ fertilizer amount × factor

Linear regression finds the best straight line through your data — the \(w_0\) and \(w_1\) that fit reality closest.

Use Cases for Linear Regression

House Price Prediction

Predict price from area, bedrooms, location

Salary Estimation

Predict salary from years of experience

Weather Forecasting

Predict temperature from historical data

Sales Forecasting

Predict revenue from ad spend

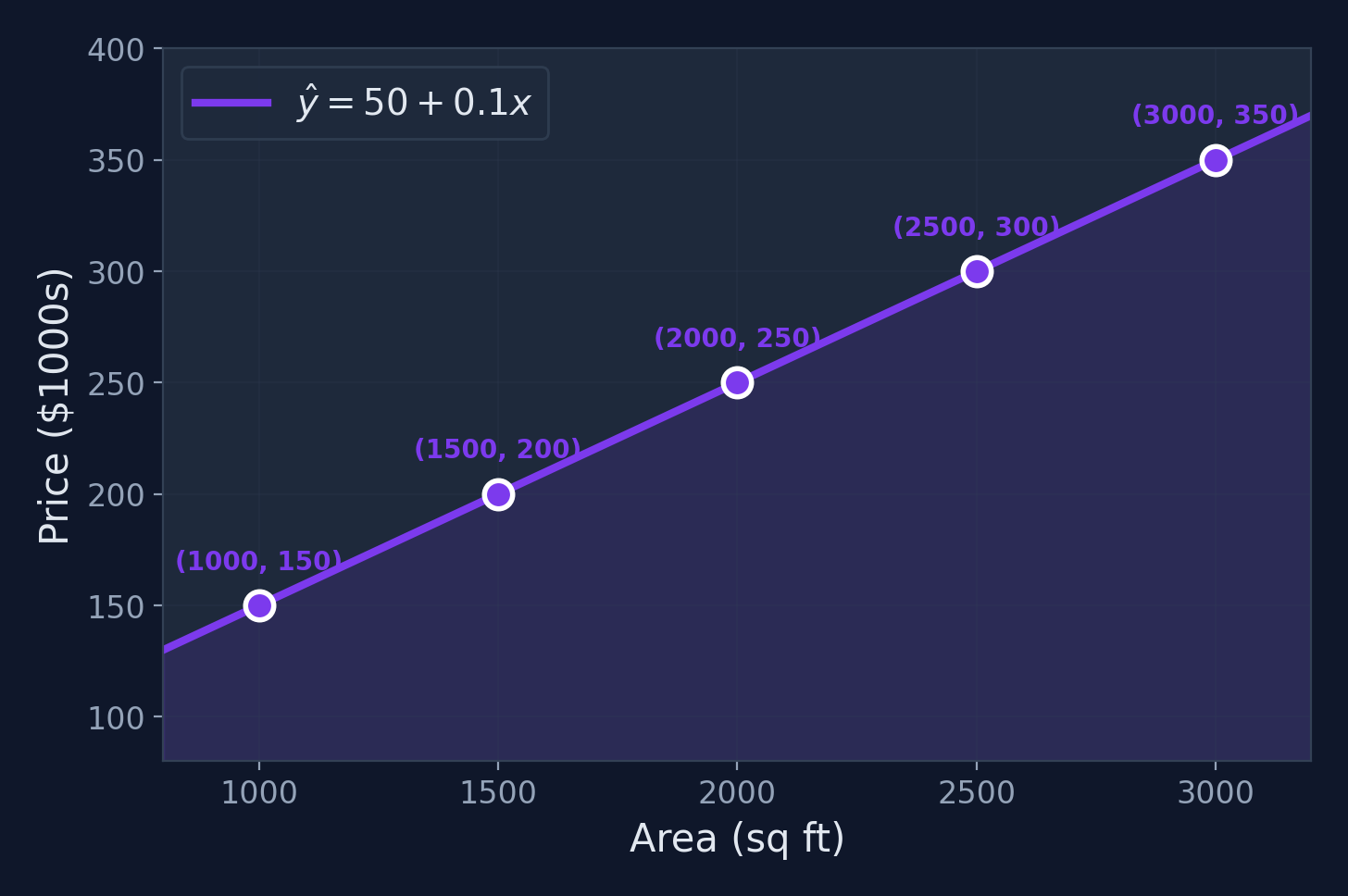

Worked Example: Setup

Problem

Predict house price ($1000s) from area (sq ft)

| Area \(x\) (sq ft) | Price \(y\) ($1000s) |

|---|---|

| 1000 | 150 |

| 1500 | 200 |

| 2000 | 250 |

| 2500 | 300 |

| 3000 | 350 |

Goal

Find \(\hat{y} = w_0 + w_1 x\) that best fits this data.

Computing the Slope \(w_1\)

$$w_1 = \frac{\sum_{i=1}^{m}(x_i - \bar{x})(y_i - \bar{y})}{\sum_{i=1}^{m}(x_i - \bar{x})^2}$$

Step 1: Compute means

\(\bar{x} = \frac{1000+1500+2000+2500+3000}{5} = 2000\)

\(\bar{y} = \frac{150+200+250+300+350}{5} = 250\)

Step 2: Compute sums

Numerator: \(250{,}000\)

Denominator: \(2{,}500{,}000\)

\(w_1 = \frac{250{,}000}{2{,}500{,}000} = \mathbf{0.1}\)

Intercept & Final Model

$$w_0 = \bar{y} - w_1 \bar{x} = 250 - 0.1 \times 2000 = \mathbf{50}$$

Final Model: \(\hat{y} = 50 + 0.1x\)

Interpretation

- Base price: $50,000 (the intercept)

- Each additional sq ft adds $100 to the price (the slope)

Making Predictions

Using our model \(\hat{y} = 50 + 0.1x\):

| Area \(x\) | Computation | Predicted Price \(\hat{y}\) |

|---|---|---|

| 1,200 sq ft | \(50 + 0.1(1200)\) | $170K |

| 1,800 sq ft | \(50 + 0.1(1800)\) | $230K |

| 2,200 sq ft | \(50 + 0.1(2200)\) | $270K |

| 3,500 sq ft | \(50 + 0.1(3500)\) | $400K |

Key

The model can predict for any area value — even ones not in the training data.

Visualization

What Does "Error" Mean?

Residuals

The vertical dashed lines are the residuals (errors): \(e_i = \hat{y}_i - y_i\). Each one measures how far off our prediction is. The "best" line minimizes these gaps overall.

Why Squared Errors?

Why not just sum the errors \(\sum(e_i)\)?

Positive and negative errors cancel out! A line through the middle of a scattered cloud could have total error = 0 despite being terrible.

Sum of errors

\(\sum e_i\)

Cancels out — useless

Absolute errors

\(\sum |e_i|\)

Works, but not differentiable at 0

Squared errors

\(\sum e_i^2\)

Always positive, differentiable, penalizes big errors more

Why "differentiable" matters

We need to take the derivative of the cost function to do gradient descent. Squared errors give us smooth derivatives — crucial for optimization.

Cost Function: Mean Squared Error

How do we measure "best fit"?

By minimizing the average squared distance between predictions and actual values.

$$J(w_0, w_1) = \frac{1}{2m}\sum_{i=1}^{m}(\hat{y}_i - y_i)^2$$

For our example

\(J = \frac{1}{10}[(150-150)^2 + (200-200)^2 + \ldots] = 0\). Perfect fit!

Next question

How do we efficiently minimize \(J\) when data isn't perfectly linear? Enter: Gradient Descent

Gradient Descent

What is Gradient Descent?

Definition

An iterative optimization algorithm that finds the minimum of a function by repeatedly taking steps proportional to the negative of the gradient.

$$w := w - \alpha \frac{\partial J}{\partial w}$$

Where \(\alpha\) is the learning rate (step size)

Intuition

Imagine standing on a foggy hill. You can only feel the slope under your feet. The gradient tells you which direction is steepest — walk the opposite way to go downhill.

Where it's used

Linear regression, logistic regression, neural networks, SVMs, transformers — virtually every ML model is trained with some form of gradient descent.

Why Do We Need Gradient Descent?

Can't we just use a formula?

For simple linear regression with 1 feature, yes — we used the closed-form formula to get \(w_1 = 0.1\). But what about...

Formula fails when...

- You have 100+ features (matrix inversion is \(O(n^3)\))

- The model is non-linear (neural networks)

- Dataset is too large for memory

GD works for...

- Any differentiable function

- Any number of parameters

- Any dataset size (mini-batches)

- Linear models and neural networks

Gradient descent is the universal optimizer — it's how we train everything from logistic regression to GPT-4.

The Calculus You Need: 3 Rules

What is a derivative?

The derivative \(\frac{df}{dx}\) tells you the slope (rate of change) of \(f\) at any point. Positive slope = function is increasing. Negative slope = decreasing.

| Rule | Formula | Example |

|---|---|---|

| Power Rule | \(\frac{d}{dx}[x^n] = nx^{n-1}\) | \(\frac{d}{dx}[x^2] = 2x\) |

| Constant Rule | \(\frac{d}{dx}[cf(x)] = c \cdot f'(x)\) | \(\frac{d}{dx}[3x^2] = 6x\) |

| Chain Rule | \(\frac{d}{dx}[f(g(x))] = f'(g(x)) \cdot g'(x)\) | \(\frac{d}{dx}[(2x+1)^2] = 2(2x+1) \cdot 2\) |

That's it!

With these 3 rules, you can derive every gradient in this lecture. Let's try it on MSE.

Intuition: Rolling Downhill

Imagine

You're standing on a hillside in dense fog. You can only feel the slope under your feet.

Strategy: Always step in the steepest downhill direction. Eventually, you reach the valley (minimum).

Why the Negative Gradient?

If gradient is negative

Subtracting a negative number = adding → we move right (toward the minimum)

If gradient is positive

Subtracting a positive number = decreasing → we move left (toward the minimum)

Either way, the negative gradient always points toward the minimum!

Use Cases for Gradient Descent

Training Neural Networks

Optimize millions of weights via backpropagation

Linear/Logistic Regression

Find optimal parameters for prediction models

Image Recognition

Train CNNs for object detection and classification

Natural Language Processing

Train transformers for language understanding

The Gradient Descent Algorithm

1. Initialize weights w randomly

2. Repeat until convergence:

a. Compute gradient: g = dJ/dw

b. Update weights: w = w - α × g

3. Return wKey insight

The gradient \(\frac{\partial J}{\partial w}\) tells us the direction of steepest ascent. We go in the opposite direction (hence the minus sign).

Deriving the MSE Gradient — Setup

Our cost function (MSE)

$$J(w_0, w_1) = \frac{1}{2m}\sum_{i=1}^{m}(\hat{y}_i - y_i)^2$$

Substitute the model

Since \(\hat{y}_i = w_0 + w_1 x_i\), we can write:

$$J(w_0, w_1) = \frac{1}{2m}\sum_{i=1}^{m}(w_0 + w_1 x_i - y_i)^2$$

We need two partial derivatives

\(\frac{\partial J}{\partial w_1}\) — how does the cost change when we adjust the slope?

\(\frac{\partial J}{\partial w_0}\) — how does the cost change when we adjust the intercept?

Deriving \(\frac{\partial J}{\partial w_1}\) — Step by Step

Step 1: Apply the derivative to the sum

$$\frac{\partial J}{\partial w_1} = \frac{1}{2m}\sum_{i=1}^{m} \frac{\partial}{\partial w_1}\left[(w_0 + w_1 x_i - y_i)^2\right]$$

Step 2: Chain rule — derivative of \((\text{something})^2\)

$$= \frac{1}{2m}\sum_{i=1}^{m} 2(w_0 + w_1 x_i - y_i) \cdot \frac{\partial}{\partial w_1}(w_0 + w_1 x_i - y_i)$$

The inner derivative w.r.t. \(w_1\): \(\frac{\partial}{\partial w_1}(w_0 + w_1 x_i - y_i) = x_i\)

Step 3: Simplify — the 2 and \(\frac{1}{2}\) cancel!

$$= \frac{1}{m}\sum_{i=1}^{m}(w_0 + w_1 x_i - y_i) \cdot x_i$$

$$\boxed{\frac{\partial J}{\partial w_1} = \frac{1}{m}\sum_{i=1}^{m}(\hat{y}_i - y_i) \cdot x_i}$$

Deriving \(\frac{\partial J}{\partial w_0}\) — Step by Step

Same process, but the inner derivative changes

$$\frac{\partial J}{\partial w_0} = \frac{1}{2m}\sum_{i=1}^{m} 2(w_0 + w_1 x_i - y_i) \cdot \frac{\partial}{\partial w_0}(w_0 + w_1 x_i - y_i)$$

Key difference

\(\frac{\partial}{\partial w_0}(w_0 + w_1 x_i - y_i) = \mathbf{1}\)

Compare: for \(w_1\) it was \(x_i\)

Result

$$\frac{\partial J}{\partial w_0} = \frac{1}{m}\sum_{i=1}^{m}(\hat{y}_i - y_i)$$

No \(x_i\) — just the average error!

Intuition: \(\frac{\partial J}{\partial w_0}\) is the average prediction error. \(\frac{\partial J}{\partial w_1}\) is the error weighted by the input — larger inputs contribute more.

The Complete Update Rules

Gradient Descent for Linear Regression

$$w_1 := w_1 - \alpha \cdot \frac{1}{m}\sum_{i=1}^{m}(\hat{y}_i - y_i) \cdot x_i$$

$$w_0 := w_0 - \alpha \cdot \frac{1}{m}\sum_{i=1}^{m}(\hat{y}_i - y_i)$$

What we derived

- Start from the cost function \(J\)

- Take partial derivatives using chain rule

- Get the gradients for each parameter

- Subtract them (scaled by \(\alpha\))

Two equations — that's it!

These two equations are all you need to train linear regression. Repeat until convergence.

GD for Linear Regression — Worked Example

Using our house price data (5 points)

Start: \(w_0 = 0,\; w_1 = 0,\; \alpha = 0.0000001\) (tiny LR because features are large)

Iteration 0: Compute predictions (\(\hat{y} = 0 + 0 \cdot x = 0\) for all)

Errors: \(\hat{y}_i - y_i = [0-150,\; 0-200,\; 0-250,\; 0-300,\; 0-350] = [-150, -200, -250, -300, -350]\)

\(\frac{\partial J}{\partial w_0}\)

\(= \frac{1}{5}(-150-200-250-300-350)\)

\(= \frac{-1250}{5} = \mathbf{-250}\)

\(\frac{\partial J}{\partial w_1}\)

\(= \frac{1}{5}[(-150)(1000) + (-200)(1500) + \ldots]\)

\(= \frac{-575{,}000}{5} \times 10^{-7} \approx \mathbf{-550{,}000}\)

Update

\(w_0' = 0 - 10^{-7}(-250) = 0.000025\), \(w_1' = 0 - 10^{-7}(-550000) = 0.055\). One step closer!

GD for Linear Regression — Convergence

| Iteration | \(w_0\) | \(w_1\) | \(J\) (cost) |

|---|---|---|---|

| 0 | 0.000 | 0.000 | 32,500 |

| 10 | 0.003 | 0.042 | 10,240 |

| 100 | 0.28 | 0.084 | 1,056 |

| 1,000 | 12.4 | 0.097 | 28.7 |

| 10,000 | 45.8 | 0.100 | 0.35 |

| ~50,000 | 50.0 | 0.100 | ≈ 0 |

Same answer!

GD converges to \(w_0 = 50,\; w_1 = 0.1\) — exactly the same as the closed-form formula.

But GD generalizes

Unlike the formula, GD works for any differentiable model — logistic regression, neural networks, transformers...

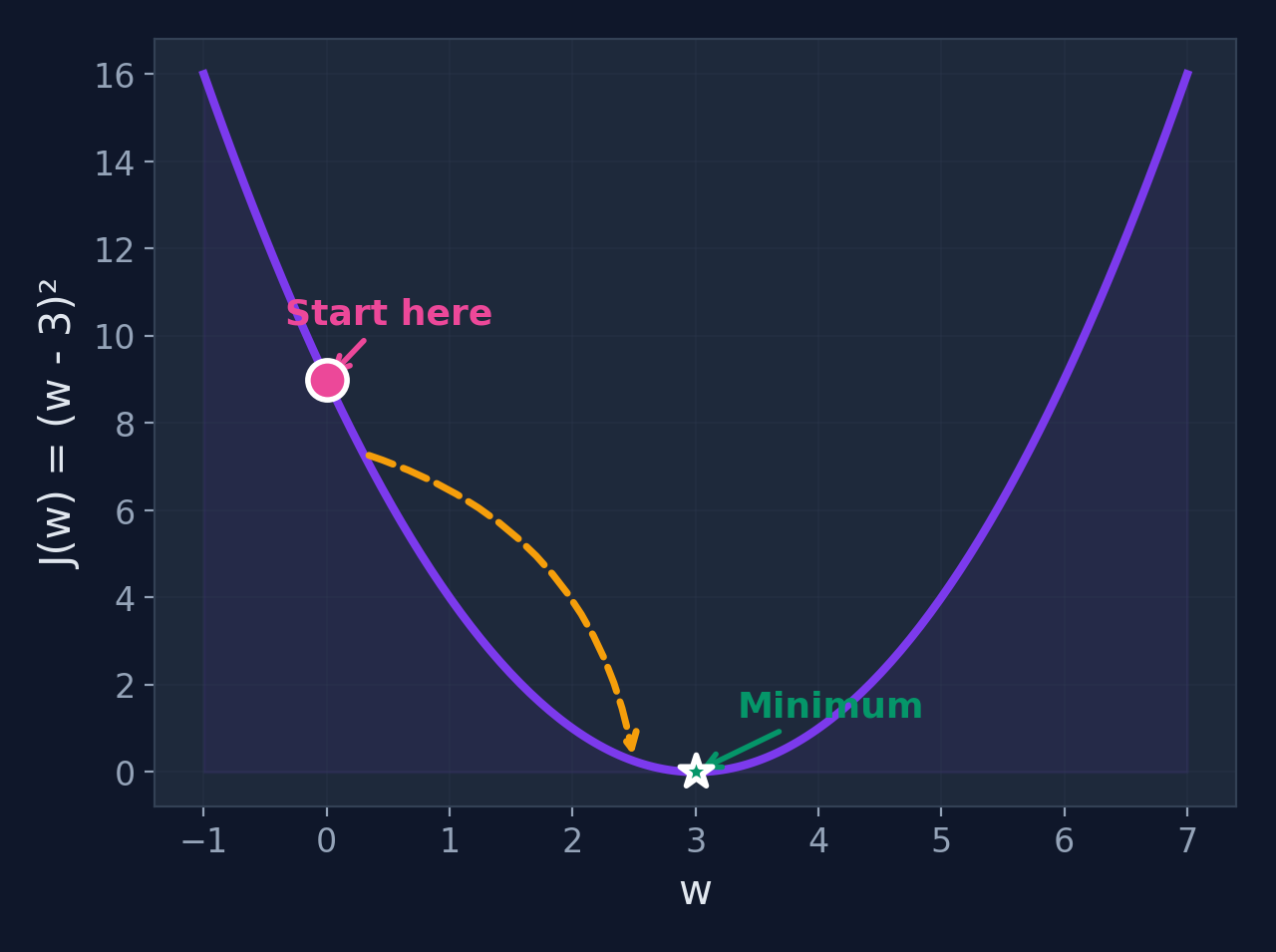

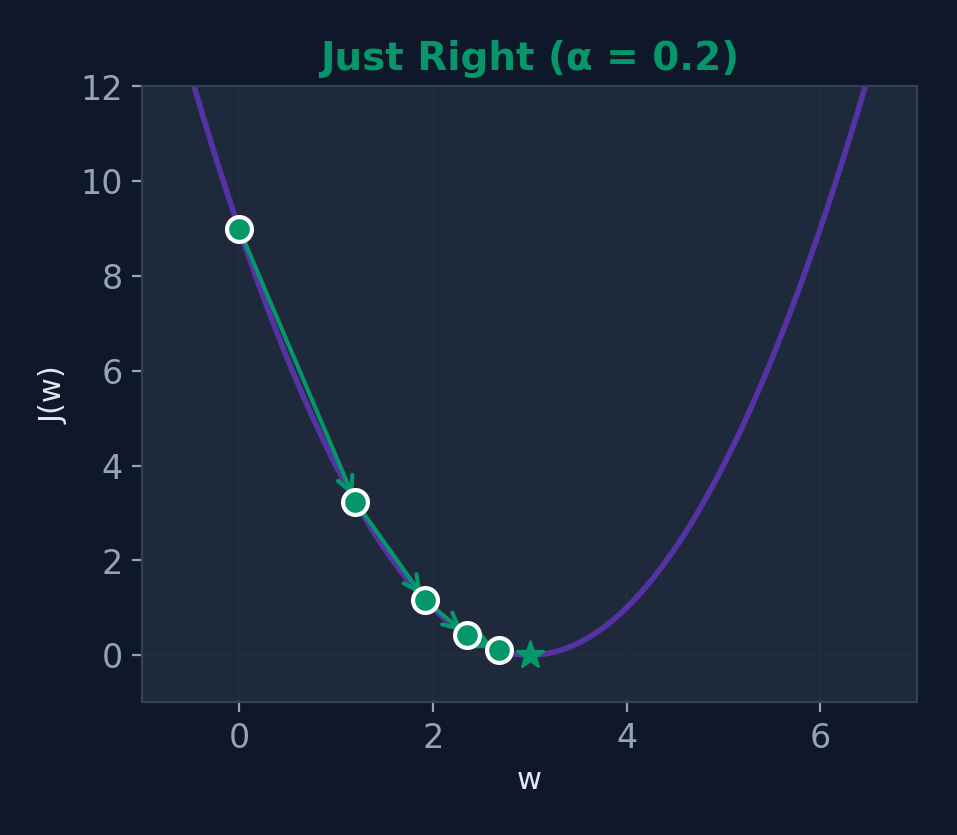

Worked Example: Setup

Problem

Minimize \(J(w) = (w - 3)^2\)

Settings

- Starting point: \(w_0 = 0\)

- Learning rate: \(\alpha = 0.2\)

- Gradient: \(\frac{dJ}{dw} = 2(w - 3)\)

Expected minimum

\(J(w)\) is minimized when \(w = 3\). Let's see if gradient descent finds it!

What we expect

Since \(J(w) = (w-3)^2\) is a perfect parabola with minimum at \(w=3\), GD should converge there. Starting at \(w=0\), the gradient is negative (slope points downhill to the right), so GD will move \(w\) to the right toward 3.

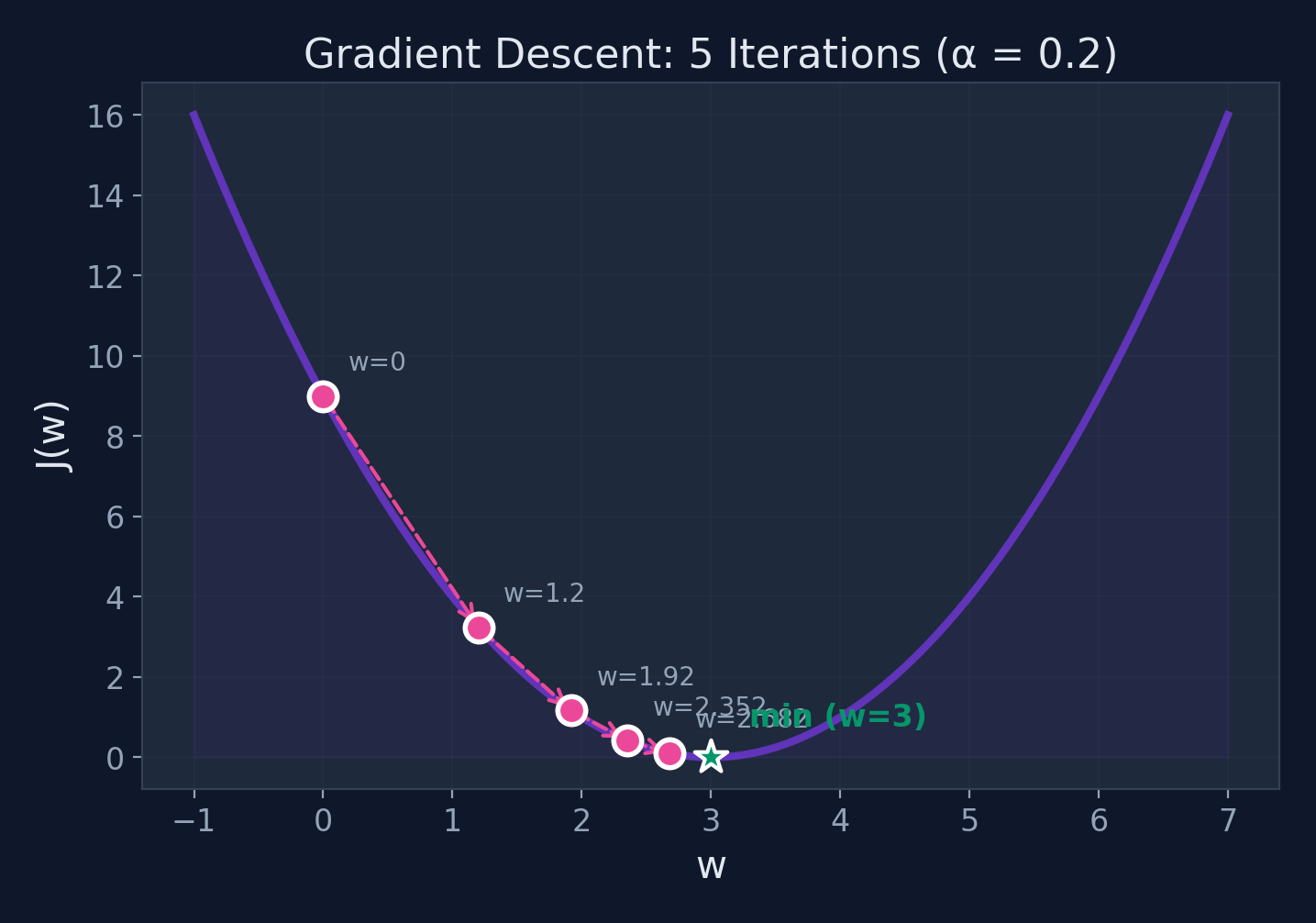

Step-by-Step Iterations

| Iter | \(w\) | \(\frac{dJ}{dw} = 2(w-3)\) | Update | New \(w\) |

|---|---|---|---|---|

| 0 | 0.000 | \(2(0-3) = -6.0\) | \(0 - 0.2(-6.0)\) | 1.200 |

| 1 | 1.200 | \(2(1.2-3) = -3.6\) | \(1.2 - 0.2(-3.6)\) | 1.920 |

| 2 | 1.920 | \(2(1.92-3) = -2.16\) | \(1.92 - 0.2(-2.16)\) | 2.352 |

| 3 | 2.352 | \(2(2.352-3) = -1.296\) | \(2.352 - 0.2(-1.296)\) | 2.611 |

| 4 | 2.611 | \(2(2.611-3) = -0.778\) | \(2.611 - 0.2(-0.778)\) | 2.767 |

Converging toward \(w = 3\)! Each step gets us closer to the minimum.

Gradient Descent in Action

Steps get smaller as we approach the minimum — the gradient decreases!

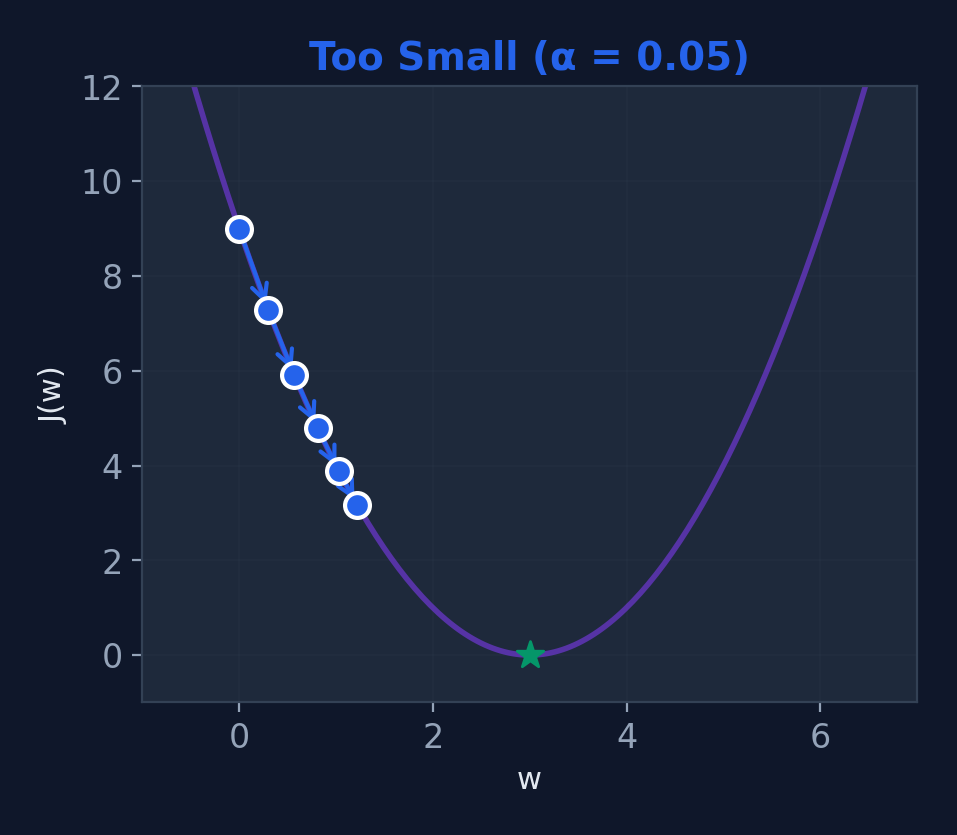

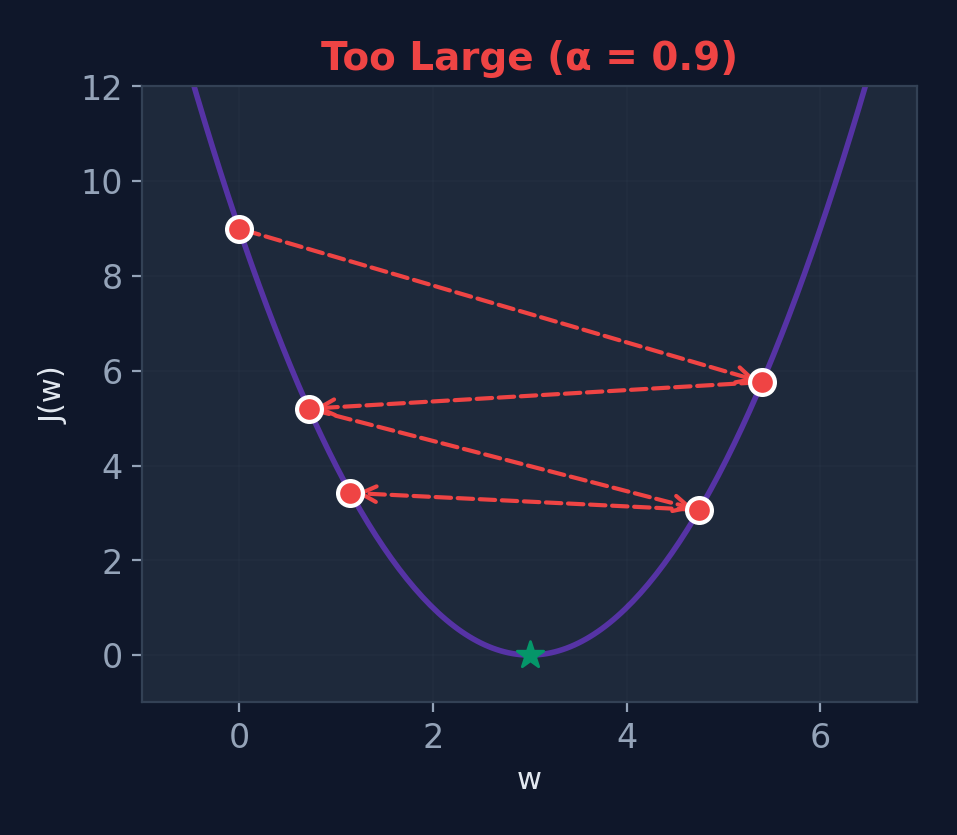

Effect of Learning Rate \(\alpha\)

Too Small (\(\alpha = 0.01\))

Slow convergence

Just Right (\(\alpha = 0.2\))

Optimal convergence

Too Large (\(\alpha = 0.9\))

Overshoots — may diverge!

Common Pitfalls

Local Minima

Non-convex functions have multiple valleys. GD might get stuck in a shallow one instead of finding the deepest.

Saddle Points

Points where gradient = 0 but it's not a minimum. The surface curves up in one direction and down in another.

Feature Scaling

If features have very different ranges (e.g., age 0–100 vs salary 0–1M), GD zig-zags instead of going straight to the minimum.

When to Stop?

Common criteria: gradient < threshold, cost change < \(\epsilon\), or fixed number of iterations.

Good news for linear regression

MSE is convex (one valley), so GD always finds the global minimum. Neural networks? Not so lucky — but it works anyway!

Gradient Descent Variants

| Variant | Data per Step | Speed | Stability |

|---|---|---|---|

| Batch GD | All samples | Slow | Very stable |

| Stochastic GD | 1 sample | Fast | Noisy |

| Mini-batch GD | \(k\) samples | Balanced | Balanced |

In practice

Mini-batch gradient descent (batch size 32–256) is the standard in deep learning. It balances speed with stable convergence.

Logistic Regression

Why Not Linear Regression for Classification?

Problem 1

Linear regression can predict -0.2 or 1.3 — what does a negative probability mean?

Problem 2

A single outlier can shift the entire line, changing the decision boundary dramatically.

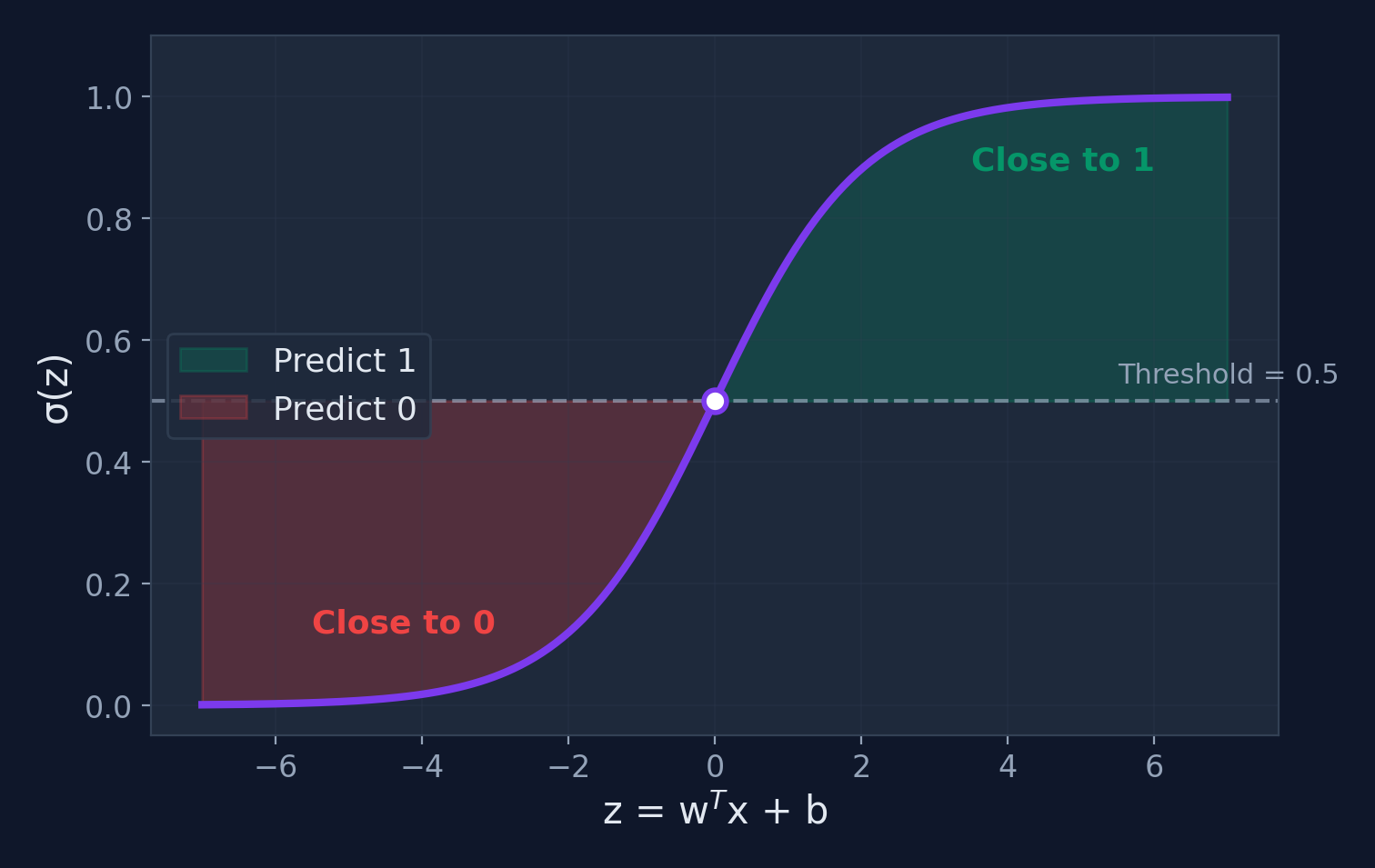

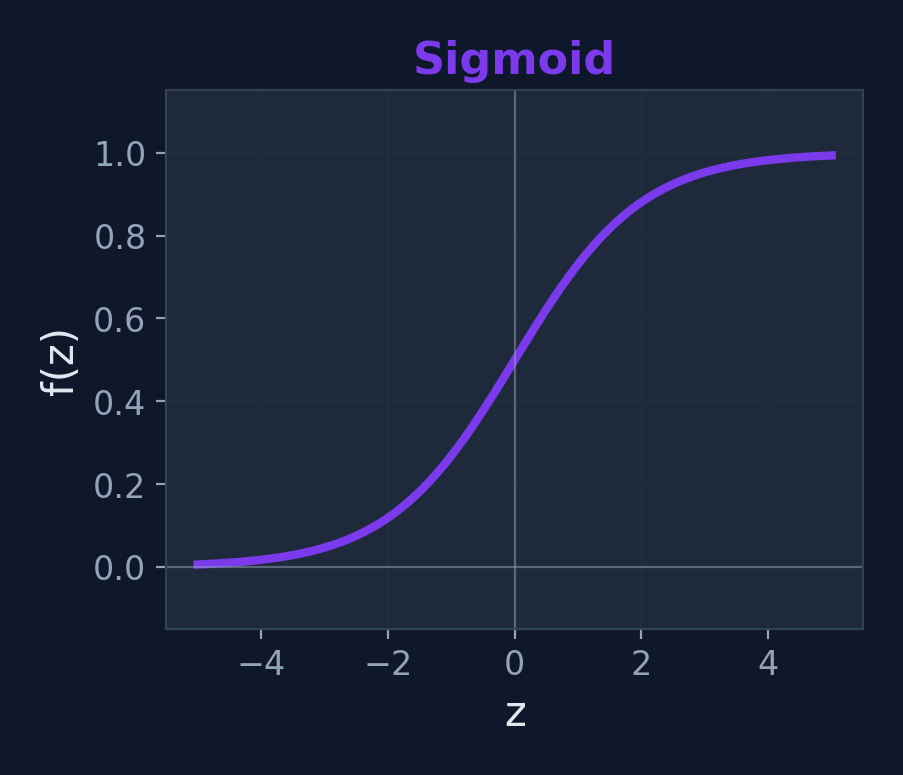

We need a function that squishes any real number into the range \((0, 1)\) → Enter: the sigmoid function

What is Logistic Regression?

Definition

A classification algorithm that models the probability of a binary outcome using the sigmoid (logistic) function.

$$\sigma(z) = \frac{1}{1 + e^{-z}}$$

$$P(y=1|\mathbf{x}) = \sigma(\mathbf{w}^T \mathbf{x} + b)$$

Key insight

The sigmoid maps any real number to \((0, 1)\) — perfect for probabilities. Output > 0.5 → class 1, otherwise class 0.

Why "logistic"?

Named after the logistic function, coined by Pierre-François Verhulst (1845) to model population growth. Same S-curve, different application!

The Sigmoid Function

Sigmoid — Computing by Hand

| \(z\) | \(e^{-z}\) | \(1 + e^{-z}\) | \(\sigma(z) = \frac{1}{1+e^{-z}}\) | Interpretation |

|---|---|---|---|---|

| \(-3\) | \(e^3 = 20.09\) | \(21.09\) | 0.047 | Very likely class 0 |

| \(-1\) | \(e^1 = 2.718\) | \(3.718\) | 0.269 | Probably class 0 |

| \(0\) | \(e^0 = 1\) | \(2\) | 0.500 | Coin flip! |

| \(1\) | \(e^{-1} = 0.368\) | \(1.368\) | 0.731 | Probably class 1 |

| \(3\) | \(e^{-3} = 0.050\) | \(1.050\) | 0.953 | Very likely class 1 |

Symmetry

\(\sigma(0) = 0.5\) always. The function is symmetric around \(z = 0\).

Saturation

For \(|z| > 5\), the sigmoid is nearly 0 or 1. The neuron is "very confident."

From Probability to Decision

Linear Combination

\(z = \mathbf{w}^T\mathbf{x} + b\)

Can be any real number

Apply Sigmoid

\(p = \sigma(z)\)

Squished to (0, 1)

Apply Threshold

\(p \geq 0.5 \rightarrow\) Class 1

\(p < 0.5 \rightarrow\) Class 0

Use Cases for Logistic Regression

Email Spam Detection

Classify emails as spam or not spam

Medical Diagnosis

Predict disease presence from symptoms

Fraud Detection

Flag suspicious credit card transactions

Student Pass/Fail

Predict outcome from study hours

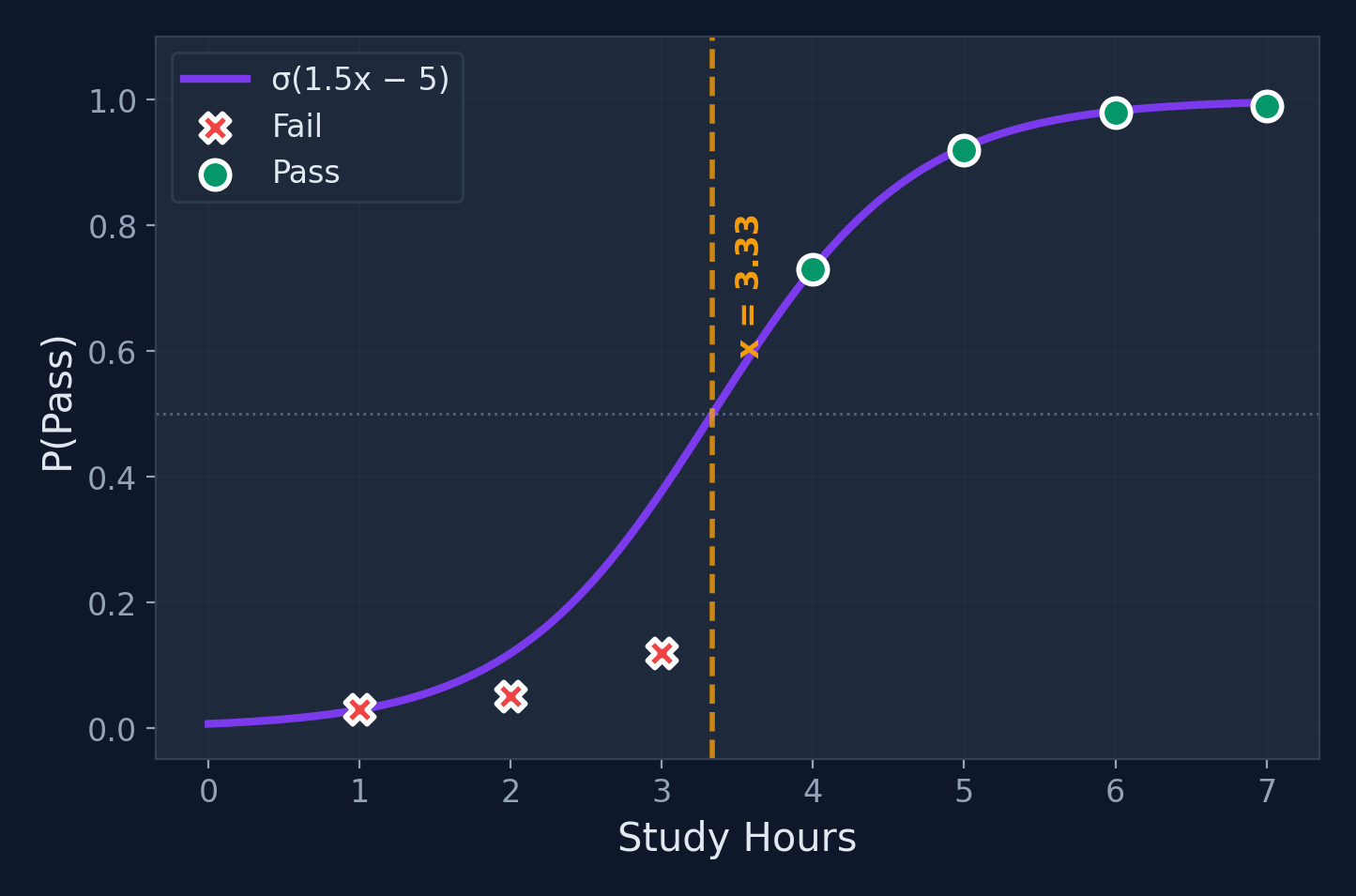

Worked Example: Setup

Problem

Predict pass/fail from study hours

| Hours \(x\) | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

|---|---|---|---|---|---|---|---|

| Result | Fail | Fail | Fail | Pass | Pass | Pass | Pass |

Assume pre-trained weights

\(w_1 = 1.5\), \(b = -5.0\). Model: \(\hat{y} = \sigma(1.5x - 5.0)\), threshold = 0.5

Forward Pass Computation

| Hours \(x\) | \(z = 1.5x - 5.0\) | \(\sigma(z) = \frac{1}{1+e^{-z}}\) | Prediction |

|---|---|---|---|

| 2 | \(1.5(2)-5 = -2.0\) | \(\frac{1}{1+e^{2.0}} = 0.119\) | Fail ✗ |

| 3 | \(1.5(3)-5 = -0.5\) | \(\frac{1}{1+e^{0.5}} = 0.378\) | Fail ✗ |

| 4 | \(1.5(4)-5 = 1.0\) | \(\frac{1}{1+e^{-1.0}} = 0.731\) | Pass ✓ |

| 5 | \(1.5(5)-5 = 2.5\) | \(\frac{1}{1+e^{-2.5}} = 0.924\) | Pass ✓ |

All predictions match! The sigmoid converts the linear score into a probability.

Loss: Binary Cross-Entropy

$$J = -\frac{1}{m}\sum_{i=1}^{m}\left[y_i \log(\hat{y}_i) + (1-y_i)\log(1-\hat{y}_i)\right]$$

Why not MSE?

MSE with sigmoid creates a non-convex loss surface with many local minima. Cross-entropy is convex — gradient descent always finds the global minimum.

Intuition

- If true label = 1 and we predict 0.01 → huge penalty

- If true label = 1 and we predict 0.99 → tiny penalty

- Penalizes confident wrong predictions heavily

Decision Boundary

Training Logistic Regression

Gradient of cross-entropy

$$\frac{\partial J}{\partial w_j} = \frac{1}{m}\sum_{i=1}^{m}(\hat{y}_i - y_i)x_j^{(i)}$$

Surprise! This looks identical to the linear regression gradient — but \(\hat{y}\) uses the sigmoid.

Training recipe

- Compute predictions: \(\hat{y} = \sigma(\mathbf{w}^T\mathbf{x} + b)\)

- Compute loss: \(J\) (cross-entropy)

- Compute gradients: \(\frac{\partial J}{\partial w}\)

- Update weights: \(w := w - \alpha \nabla J\)

- Repeat until convergence

Linear vs Logistic Regression

| Feature | Linear Regression | Logistic Regression |

|---|---|---|

| Output | Continuous value | Probability (0–1) |

| Activation | None (identity) | Sigmoid |

| Loss Function | Mean Squared Error | Binary Cross-Entropy |

| Use Case | Regression (predict amount) | Classification (predict class) |

| Decision | No threshold | Threshold at 0.5 |

Key insight

Logistic regression is essentially linear regression + sigmoid. This idea of "linear combination + activation" is the foundation of neural networks!

Regularization

What is Regularization?

Definition

A technique that adds a penalty term to the loss function to prevent overfitting by discouraging overly complex models.

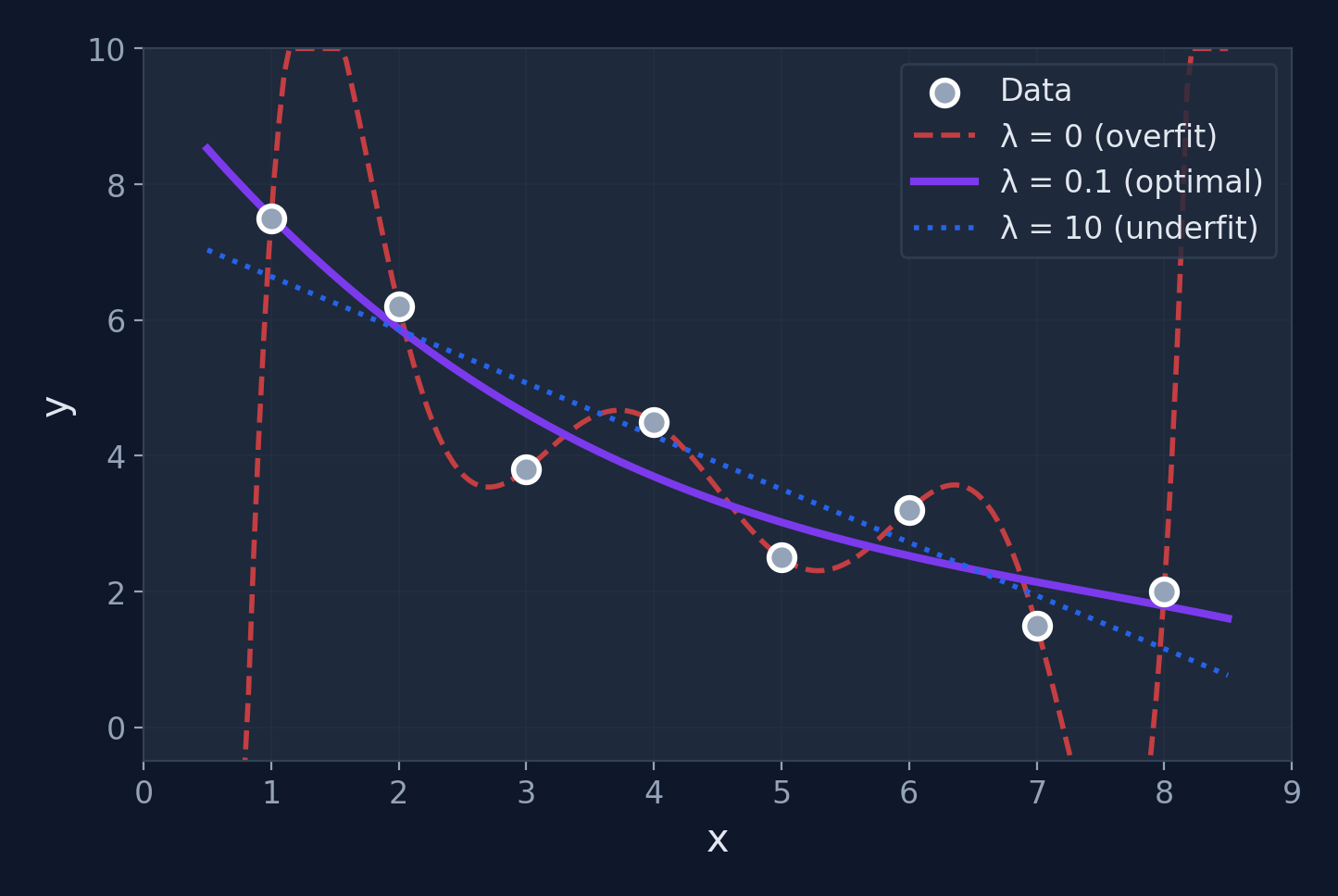

$$J_{\text{reg}} = J_{\text{original}} + \lambda \cdot R(\mathbf{w})$$

Where \(\lambda\) controls regularization strength

Think of it as...

Regularization is like a teacher telling a student: "I don't just want the right answer — I want a simple explanation." Simpler models generalize better.

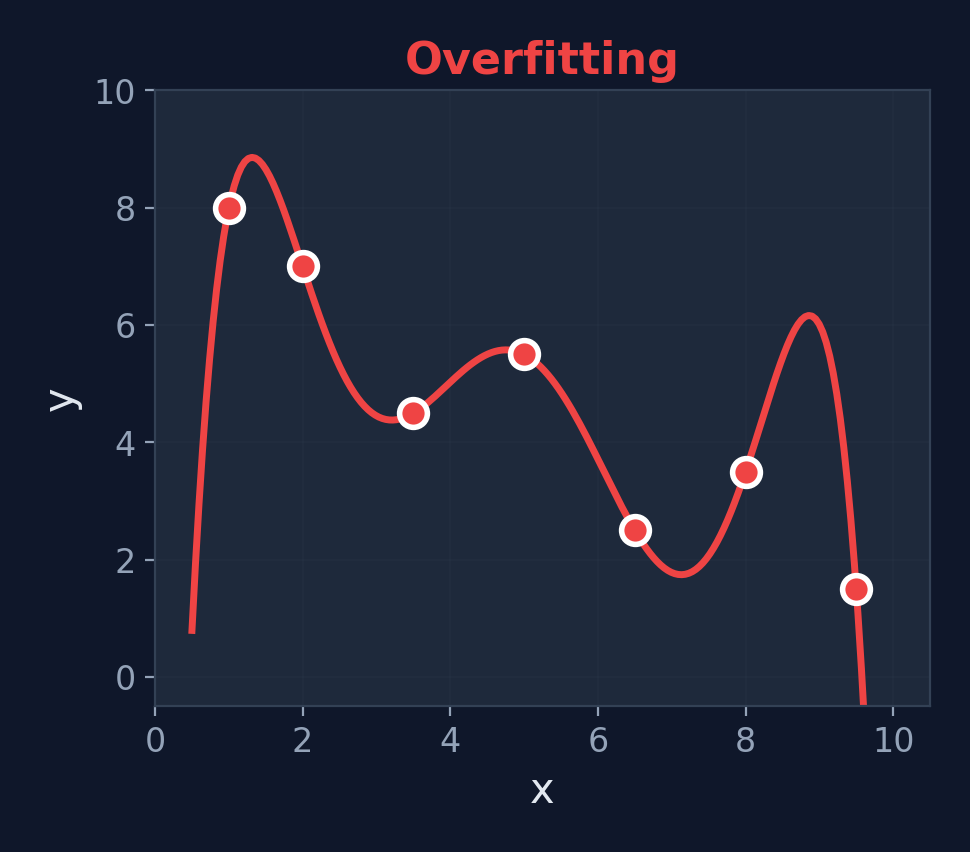

Without regularization

Models may memorize training data instead of learning general patterns — performing perfectly on training data but failing on new data.

The \(\lambda\) dial

\(\lambda = 0\): no penalty (may overfit). \(\lambda \to \infty\): all weights → 0 (underfits). Cross-validation finds the sweet spot.

The Overfitting Analogy

The Memorizer

Memorizes every answer from past exams word-for-word

The Understander

Learns the underlying concepts and problem-solving strategies

Regularization forces the model to "understand" rather than "memorize" — slightly worse on training data, much better on new data.

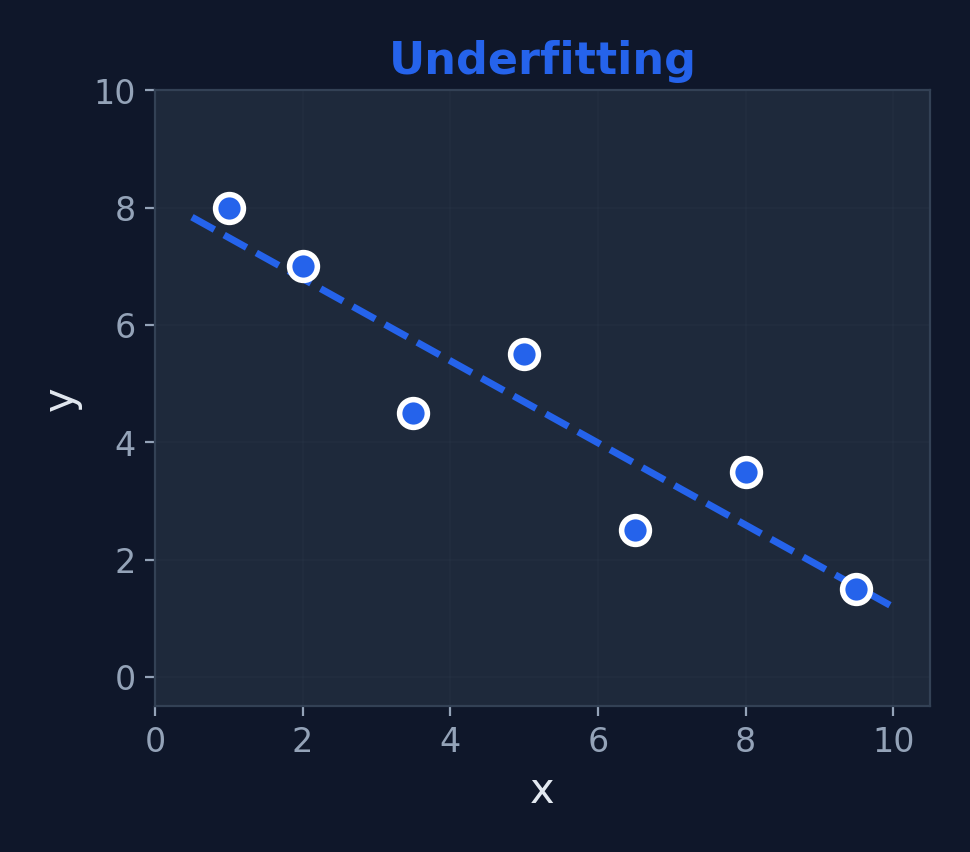

Underfitting vs. Just Right vs. Overfitting

Underfitting

High Bias — too simple

Just Right

Good Balance

Overfitting

High Variance — too complex

Types of Regularization

L1 Regularization (Lasso)

$$J_{L1} = J + \lambda \sum_{i} |w_i|$$

Encourages sparsity — some weights become exactly 0, effectively performing feature selection.

L2 Regularization (Ridge)

$$J_{L2} = J + \lambda \sum_{i} w_i^2$$

Shrinks all weights toward 0 but never exactly 0. Smoother, more stable solutions.

When to use L1

You suspect many features are irrelevant and want the model to automatically ignore them. L1 acts as a built-in feature selector.

When to use L2

All features matter but you want to prevent any single weight from dominating. L2 keeps everything small and balanced — the default choice.

Beyond L1 & L2: More Techniques

Elastic Net (L1 + L2)

$$J_{EN} = J + \lambda_1 \sum|w_i| + \lambda_2 \sum w_i^2$$

Combines the best of both: feature selection and weight shrinkage. Used in scikit-learn's ElasticNet.

Dropout (Neural Networks)

Randomly "turn off" neurons during training (e.g., 50% chance). Forces the network to not rely on any single neuron.

Like studying with random pages removed — you learn the core concepts, not surface patterns.

Preview

We'll explore dropout in detail when we cover deep network training. For now, remember: regularization = adding constraints to prevent overfitting.

Use Cases for Regularization

Feature Selection (L1)

Automatically remove irrelevant features by zeroing their weights

Neural Network Training

Prevent deep networks from memorizing training data

Reducing Complexity

Keep models simple and interpretable

Improving Generalization

Models perform better on unseen test data

Worked Example: L2 Regularization

Applying L2 penalty to our linear regression

Original model: \(w_0 = 50\) (bias), \(w_1 = 0.1\) (weight), and \(\lambda = 0.01\)

Without regularization

\(J = 0\) (perfect fit)

With L2 regularization

\(J_{\text{reg}} = 0 + 0.01 \times (0.1^2) = 0 + 0.01 \times 0.01 = \mathbf{0.0001}\)

Updated gradient

\(\frac{\partial J_{\text{reg}}}{\partial w_j} = \frac{\partial J}{\partial w_j} + 2\lambda w_j\) — only feature weights; bias \(w_0\) is not penalized. The penalty pushes large weights smaller during training.

Effect of \(\lambda\)

Regularization Summary

Key Takeaways

- Regularization controls model complexity via a penalty term

- L1 (Lasso): Feature selection (sparse weights)

- L2 (Ridge): Weight shrinkage (smooth models)

- \(\lambda\) balances fit quality vs. complexity

- Elastic Net: Combines L1 + L2 (best of both)

What's Next?

We now have the classical building blocks:

- Regression (linear & logistic)

- Optimization (gradient descent)

- Regularization (preventing overfitting)

Let's look at the history that led from these ideas to neural networks...

Cheat Sheet

| Method | Penalty | Effect | Best for |

|---|---|---|---|

| L1 | \(\lambda\sum|w_i|\) | Zeros out weights | Feature selection |

| L2 | \(\lambda\sum w_i^2\) | Shrinks weights | Preventing large weights |

| Elastic Net | L1 + L2 | Both | Correlated features |

| Dropout | Random neuron removal | Ensemble effect | Neural networks |

A Brief History of Neural Networks

From the 1940s to Today

The Early Years (1943–1969)

McCulloch & Pitts — First mathematical model of an artificial neuron. Showed neurons could compute logical functions.

Frank Rosenblatt's Perceptron — First trainable neural network, implemented in hardware. Could learn to classify simple patterns.

Minsky & Papert — Published "Perceptrons", proving single-layer networks cannot solve XOR. Revealed fundamental limitations.

First AI Winter (1970s)

Funding and interest dried up. Neural network research was largely abandoned for over a decade.

The Resurgence (1986–2006)

Rumelhart, Hinton & Williams — Popularized backpropagation, enabling training of multi-layer networks. The key breakthrough.

Yann LeCun — Applied CNNs to handwritten digit recognition (MNIST). First practical deep learning success.

Hochreiter & Schmidhuber — Invented LSTM for sequential data, solving the vanishing gradient problem.

Geoffrey Hinton — Deep Belief Networks. The term "Deep Learning" enters mainstream AI vocabulary.

Why backpropagation mattered

Before 1986, there was no efficient way to train multi-layer networks. Backpropagation gave us a systematic method to compute gradients for every weight — not just the output layer, but all hidden layers too. This was the missing piece.

The Deep Learning Era (2012–Present)

AlexNet wins ImageNet by a huge margin. 8 layers, GPU training. The "Big Bang" of modern deep learning.

GANs (Goodfellow) — Generative Adversarial Networks can create realistic images from noise.

"Attention Is All You Need" — The Transformer architecture revolutionizes NLP and later all of AI.

ChatGPT & LLMs — Large language models reach mainstream. AI becomes a daily tool for millions.

Why Neural Networks Work Now

Big Data

Internet, smartphones, and sensors generate massive datasets. Deep networks need lots of data to learn effectively.

Compute Power

GPUs, TPUs, and cloud computing make training billion-parameter models feasible. 10,000x faster than 2000s hardware.

Better Algorithms

ReLU, batch normalization, dropout, residual connections, Adam optimizer — all invented in the 2010s.

From Classical ML to Neural Networks

Everything connects

A neural network is built from the same building blocks we've been studying — weighted sums, activation functions, and gradient-based optimization.

Think-Pair-Share

Discussion Question

Why did neural networks fail in the 1970s but succeed in the 2010s?

What changed in terms of data, compute, and algorithms?

Hint: Data

How much data existed in the 1970s vs. the age of the internet?

Hint: Compute

What hardware breakthrough made matrix multiplication 100× faster?

Hint: Algorithms

What training method was missing before 1986?

Click to reveal answer

1970s: Limited data, no GPUs, only single-layer networks (couldn't solve XOR). 2010s: Internet-scale data, GPU parallelism (NVIDIA CUDA), and breakthroughs like backpropagation, ReLU, and batch normalization made deep networks trainable.

The Simple Neuron

The Perceptron

What is an Artificial Neuron?

Definition

A computational unit that takes weighted inputs, sums them, adds a bias, and applies an activation function.

$$z = \sum_{i=1}^{n} w_i x_i + b, \quad a = f(z)$$

Biological vs. Artificial

Mapping

| Dendrites | → Inputs \(x_1, x_2, \ldots\) |

| Synaptic strength | → Weights \(w_1, w_2, \ldots\) |

| Soma (cell body) | → Summation \(\Sigma\) |

| Axon hillock | → Activation function \(f\) |

| Axon | → Output \(\hat{y}\) |

Important caveat

Real neurons are vastly more complex — they use timing, chemical signals, and recurrent connections. The artificial neuron is a very rough approximation.

Common Activation Functions

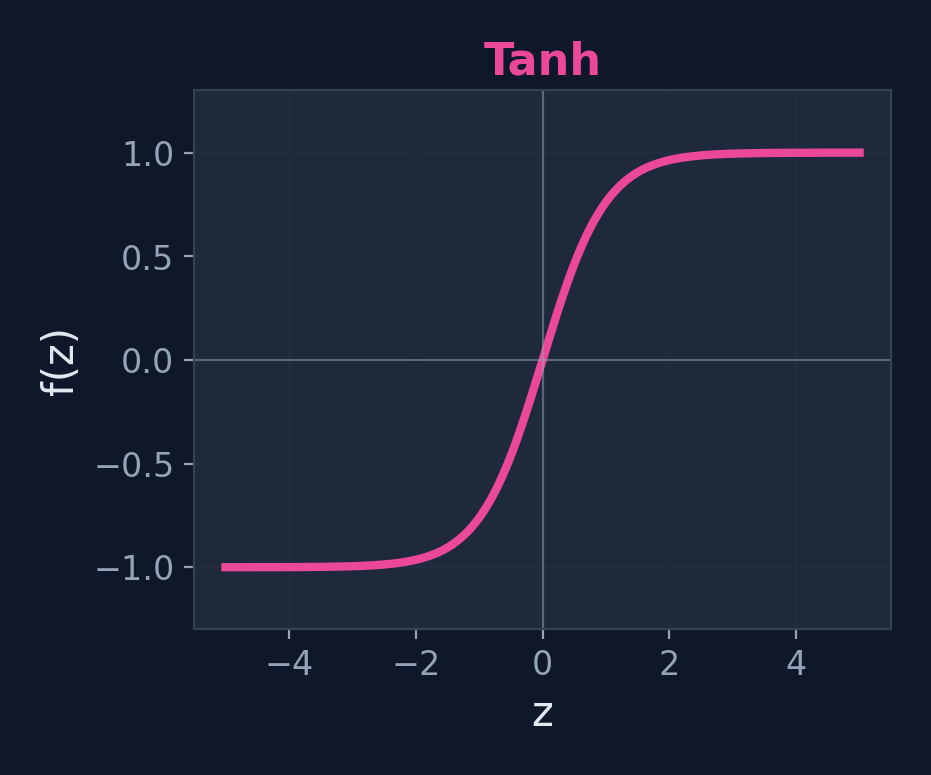

Sigmoid

\(f(z) = \frac{1}{1+e^{-z}}\)

Range: (0, 1)

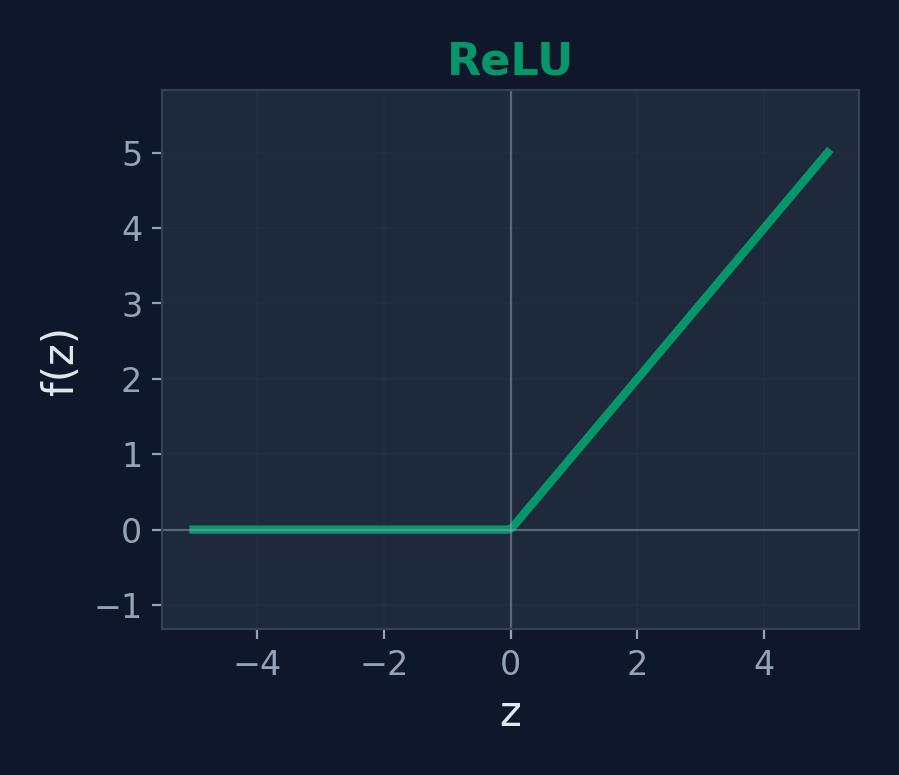

ReLU

\(f(z) = \max(0, z)\)

Range: [0, ∞)

Tanh

\(f(z) = \tanh(z)\)

Range: (-1, 1)

Modern default: ReLU

Fast to compute, avoids vanishing gradient problem, works well in practice.

What Can a Single Neuron Do?

Key Insight

A single neuron with sigmoid activation is logistic regression! Same weighted sum + same activation function.

Capabilities

- Binary classification

- Logic gates: AND, OR, NOT

- Any linearly separable problem

Limitations

- Cannot solve XOR

- Cannot learn non-linear boundaries

- Only one decision boundary (a line/plane)

Worked Example: AND Gate

Neuron

\(w_1 = 1,\; w_2 = 1,\; b = -1.5\), step activation \(f(z) = \begin{cases}1 & z \geq 0\\0 & z < 0\end{cases}\)

| \(x_1\) | \(x_2\) | \(z = x_1 + x_2 - 1.5\) | \(f(z)\) | AND | Match? |

|---|---|---|---|---|---|

| 0 | 0 | \(0 + 0 - 1.5 = -1.5\) | 0 | 0 | ✓ |

| 0 | 1 | \(0 + 1 - 1.5 = -0.5\) | 0 | 0 | ✓ |

| 1 | 0 | \(1 + 0 - 1.5 = -0.5\) | 0 | 0 | ✓ |

| 1 | 1 | \(1 + 1 - 1.5 = 0.5\) | 1 | 1 | ✓ |

The perceptron correctly computes AND! A single neuron can learn any linearly separable function.

OR Gate — Change the Bias!

Neuron

\(w_1 = 1,\; w_2 = 1,\; b = -0.5\), same step activation

| \(x_1\) | \(x_2\) | \(z = x_1 + x_2 - 0.5\) | \(f(z)\) | OR | Match? |

|---|---|---|---|---|---|

| 0 | 0 | \(0 + 0 - 0.5 = -0.5\) | 0 | 0 | ✓ |

| 0 | 1 | \(0 + 1 - 0.5 = 0.5\) | 1 | 1 | ✓ |

| 1 | 0 | \(1 + 0 - 0.5 = 0.5\) | 1 | 1 | ✓ |

| 1 | 1 | \(1 + 1 - 0.5 = 1.5\) | 1 | 1 | ✓ |

Just by changing the bias from \(-1.5\) to \(-0.5\), the neuron switches from AND to OR!

NOT Gate — Single Input

Neuron

\(w_1 = -1,\; b = 0.5\), step activation. Only one input.

| \(x\) | \(z = -x + 0.5\) | \(f(z)\) | NOT \(x\) | Match? |

|---|---|---|---|---|

| 0 | \(-0 + 0.5 = 0.5\) | 1 | 1 | ✓ |

| 1 | \(-1 + 0.5 = -0.5\) | 0 | 0 | ✓ |

Key insight

With AND, OR, and NOT, neurons can compute any Boolean function... if we stack them in layers.

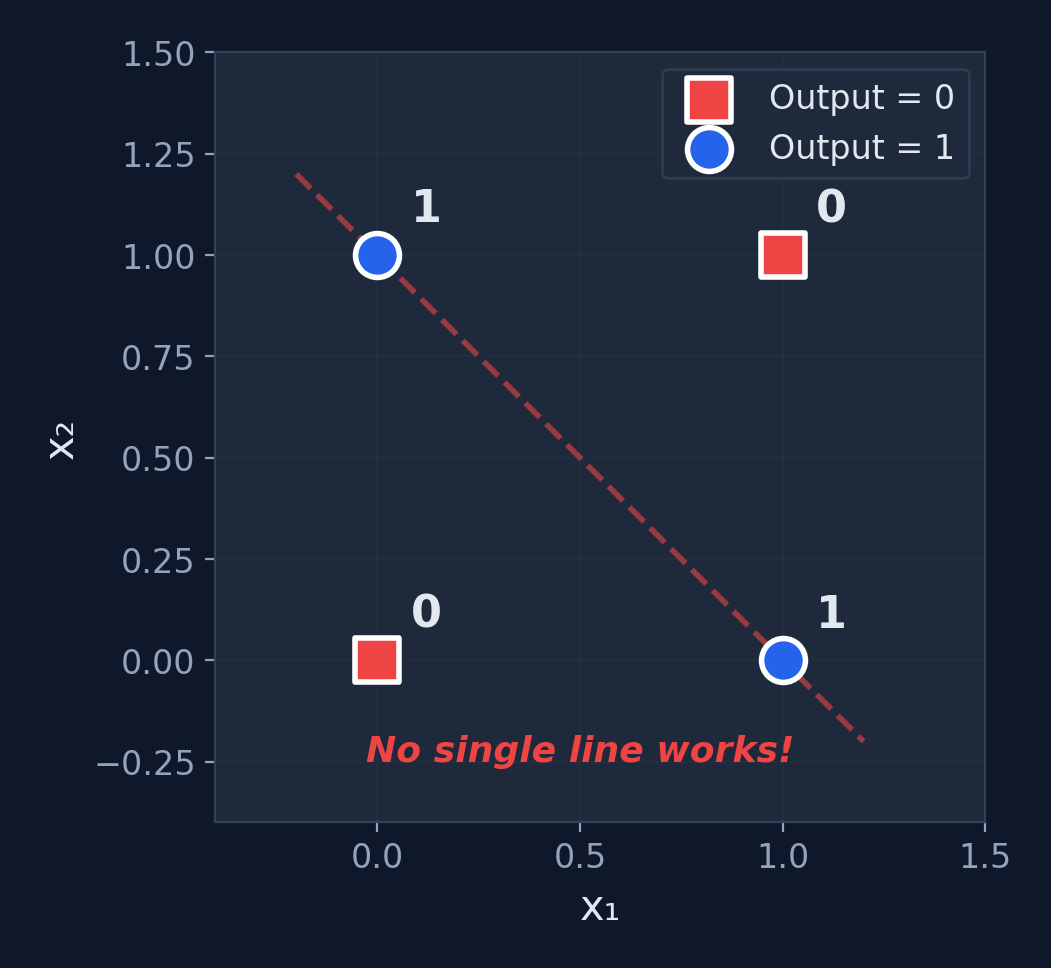

The XOR Problem

Can a single neuron compute XOR?

| \(x_1\) | \(x_2\) | XOR |

|---|---|---|

| 0 | 0 | 0 |

| 0 | 1 | 1 |

| 1 | 0 | 1 |

| 1 | 1 | 0 |

No! XOR is not linearly separable. No single straight line can separate the 1s from the 0s.

AND Gate Neuron — Traced

Step-by-step for input (1, 1)

- \(z = w_1 x_1 + w_2 x_2 + b\)

- \(z = 1(1) + 1(1) + (-1.5)\)

- \(z = 2 - 1.5 = 0.5\)

- \(f(0.5) = 1\) (since \(0.5 \geq 0\))

Output: 1 ✓ Correct!

We Need More Power

The Limitation

A single neuron can only learn linearly separable patterns. It draws one straight line through feature space.

The Solution

Stack multiple neurons in layers. Each neuron learns a different feature. Together, they can solve XOR and any non-linear problem!

Enter: The Multilayer Perceptron (MLP)

Mathematical proof

Minsky & Papert (1969) formally proved no single perceptron can solve XOR. This wasn't opinion — it was a theorem. The search for multilayer networks was the direct response.

The key insight

One hidden neuron can learn one decision boundary. Two hidden neurons = two boundaries. Combined, they carve out any region in feature space.

Multilayer Perceptron

Hidden Layers

What is an MLP?

Definition

A feedforward neural network with one or more hidden layers between the input and output layers. Each layer is fully connected to the next.

Structure

Input Layer → Hidden Layer(s) → Output Layer

- Each connection has a weight

- Each neuron has a bias and activation function

- Information flows forward only (no loops)

Universal Approximation Theorem

An MLP with just one hidden layer (enough neurons) can approximate any continuous function. This was proven by Cybenko in 1989.

Terminology

Feedforward = data flows one direction. Dense layer = fully connected layer. Hidden = not directly observed (neither input nor output).

What Hidden Layers Actually Learn

Layer 1: Edges

Detects simple patterns — lines, curves, light/dark transitions

Layer 2: Parts

Combines edges into shapes — eyes, noses, wheels, letters

Layer 3: Objects

Combines parts into concepts — faces, cars, words

Key insight

Each layer builds more abstract representations from the layer before. The network automatically learns what features matter — no manual feature engineering needed.

MLP Architecture

Reading the diagram

Each circle = a neuron. Each line = a weight. Blue = inputs, purple = hidden neurons, green = output.

Parameter count

Weights: \(2 \times 3 + 3 \times 1 = 9\). Biases: \(3 + 1 = 4\). Total: 13 parameters.

Use Cases for MLP

XOR & Non-Linear Classification

Solve problems that single neurons cannot

Handwritten Digit Recognition

MNIST dataset — the "Hello World" of deep learning

Function Approximation

Universal approximation theorem: can approximate any continuous function

Tabular Data Prediction

Structured data with complex feature interactions

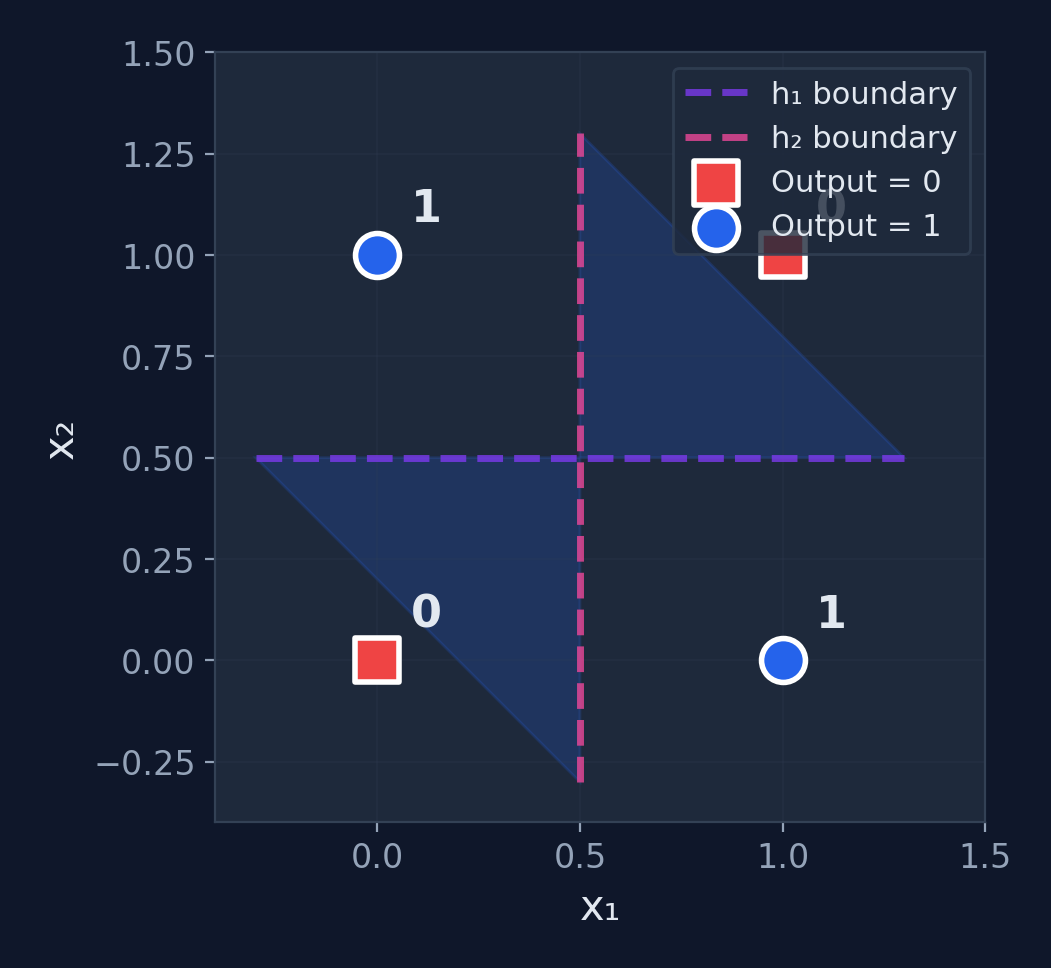

Solving XOR with an MLP

Network

2 inputs, 2 hidden neurons (step activation), 1 output

Hidden neuron \(h_1\) (OR-like)

\(w_{11}=1,\; w_{12}=1,\; b_1=-0.5\)

\(h_1 = f(x_1 + x_2 - 0.5)\)

Hidden neuron \(h_2\) (AND)

\(w_{21}=1,\; w_{22}=1,\; b_2=-1.5\)

\(h_2 = f(x_1 + x_2 - 1.5)\)

Output neuron

\(v_1 = 1,\; v_2 = -2,\; b_o = -0.5\). \(\hat{y} = f(h_1 - 2h_2 - 0.5)\) — computes "\(h_1\) AND NOT \(h_2\)"

XOR — Full Computation

| \(x_1\) | \(x_2\) | \(h_1\) = f(\(x_1+x_2-0.5\)) | \(h_2\) = f(\(x_1+x_2-1.5\)) | \(\hat{y}\) = f(\(h_1-2h_2-0.5\)) | XOR | |

|---|---|---|---|---|---|---|

| 0 | 0 | f(-0.5) = 0 | f(-1.5) = 0 | f(-0.5) = 0 | 0 | ✓ |

| 0 | 1 | f(0.5) = 1 | f(-0.5) = 0 | f(0.5) = 1 | 1 | ✓ |

| 1 | 0 | f(0.5) = 1 | f(-0.5) = 0 | f(0.5) = 1 | 1 | ✓ |

| 1 | 1 | f(1.5) = 1 | f(0.5) = 1 | f(-1.5) = 0 | 0 | ✓ |

XOR Solved! The hidden layer creates intermediate features that make the problem linearly separable.

Backpropagation: The Key Idea

The Problem

We know the output is wrong, but how do we know which hidden weights to blame? The hidden neurons don't have direct targets — only the output does.

Factory Analogy

Imagine a factory assembly line with 3 stations. The final product is defective. You trace backward:

- Station 3 (output): added the wrong label → fix station 3

- Station 2 (hidden): provided a bent component → fix station 2

- Station 1 (hidden): cut the material too short → fix station 1

Backpropagation does exactly this — it traces the error backward through each layer.

The math tool that makes this possible: the chain rule from calculus.

Training MLPs: Backpropagation

Forward Pass

- Feed input through network

- Compute each layer's output

- Get final prediction \(\hat{y}\)

- Compute loss \(J\)

Backward Pass

- Compute output error

- Propagate error backward

- Compute gradients via chain rule

- Update all weights

Chain Rule

$$\frac{\partial J}{\partial w^{[l]}} = \frac{\partial J}{\partial a^{[L]}} \cdot \frac{\partial a^{[L]}}{\partial z^{[L]}} \cdot \ldots \cdot \frac{\partial z^{[l]}}{\partial w^{[l]}}$$

Backpropagation = the chain rule applied systematically across layers

Backprop Example: Forward Pass

Tiny network: 1 input → 1 hidden (sigmoid) → 1 output (sigmoid)

Input: \(x = 1\), Target: \(y = 1\), Learning rate: \(\alpha = 0.5\)

Weights: \(w_1 = 0.5,\; b_1 = 0.2\) (hidden) | \(w_2 = 0.8,\; b_2 = 0.1\) (output)

Hidden layer

\(z_1 = w_1 x + b_1 = 0.5(1) + 0.2 = 0.7\)

\(h = \sigma(0.7) = \frac{1}{1+e^{-0.7}} = \mathbf{0.668}\)

Output layer

\(z_2 = w_2 h + b_2 = 0.8(0.668) + 0.1 = 0.634\)

\(\hat{y} = \sigma(0.634) = \frac{1}{1+e^{-0.634}} = \mathbf{0.653}\)

Loss (MSE)

\(L = \frac{1}{2}(\hat{y} - y)^2 = \frac{1}{2}(0.653 - 1)^2 = \frac{1}{2}(0.121) = \mathbf{0.0603}\). We want to reduce this!

Backprop Example: Backward Pass

Output layer gradient (\(\frac{\partial L}{\partial w_2}\))

\(\frac{\partial L}{\partial \hat{y}} = \hat{y} - y = 0.653 - 1 = -0.347\)

\(\frac{\partial \hat{y}}{\partial z_2} = \hat{y}(1-\hat{y}) = 0.653 \times 0.347 = 0.2266\) (sigmoid derivative)

\(\frac{\partial z_2}{\partial w_2} = h = 0.668\)

Chain rule: \(\frac{\partial L}{\partial w_2} = (-0.347)(0.2266)(0.668) = \mathbf{-0.0525}\)

Hidden layer gradient (\(\frac{\partial L}{\partial w_1}\))

Continue the chain through \(w_2\): \(\frac{\partial z_2}{\partial h} = w_2 = 0.8\), \(\frac{\partial h}{\partial z_1} = h(1-h) = 0.668 \times 0.332 = 0.2218\), \(\frac{\partial z_1}{\partial w_1} = x = 1\)

Chain rule: \(\frac{\partial L}{\partial w_1} = (-0.347)(0.2266)(0.8)(0.2218)(1) = \mathbf{-0.01394}\)

Backprop Example: Update & Verify

Update weights (\(\alpha = 0.5\))

\(w_2' = 0.8 - 0.5(-0.0525) = \mathbf{0.826}\)

\(w_1' = 0.5 - 0.5(-0.01394) = \mathbf{0.507}\)

Verify: new forward pass

\(z_1' = 0.507(1) + 0.2 = 0.707\)

\(h' = \sigma(0.707) = 0.670\)

\(z_2' = 0.826(0.670) + 0.1 = 0.653\)

\(\hat{y}' = \sigma(0.653) = \mathbf{0.658}\)

One step of backprop reduced the loss! Repeat this thousands of times and the network learns.

How the MLP Solves XOR

What happened?

- \(h_1\) draws one boundary line

- \(h_2\) draws another boundary line

- The output combines them: the region between the lines is class 1

- Two linear boundaries → one non-linear decision region

The power of hidden layers

They transform the input space into a representation where the problem becomes linearly separable.

Fully Connected Neural Networks

Going Deep

What is a Fully Connected Neural Network?

Definition

A deep neural network where every neuron in one layer is connected to every neuron in the next layer. Also called a Dense Network or Deep Feedforward Network.

MLP vs FCNN

An MLP with 2+ hidden layers = a Fully Connected Neural Network. "Deep" means multiple hidden layers.

Key property

More layers = more abstraction. Early layers learn simple features, deeper layers learn complex combinations.

Why "deep"?

A network with 2+ hidden layers is called "deep." More depth = more capacity to learn complex patterns. Most modern networks have 10–100+ layers.

Scale comparison

Our XOR solver: 2 layers, 13 params. MNIST digit recognizer: 2 layers, 109K params. GPT-4: ~120 layers, 1.8T params.

FCNN Architecture

Parameters: \((3 \times 4 + 4) + (4 \times 4 + 4) + (4 \times 2 + 2) = 16 + 20 + 10 = \mathbf{46}\) total

How Many Operations? Thinking About Scale

Every parameter = 1 multiply + 1 add

A forward pass through a network requires one multiplication per weight and one addition per bias. The total cost scales with parameter count.

Why GPUs matter

A CPU does operations one-by-one. A GPU does thousands in parallel. Training GPT-4 on a single CPU would take ~300 years. On 25,000 GPUs: ~3 months.

Use Cases for FCNNs

Image Classification

Flatten pixels into a vector and classify (before CNNs took over)

Natural Language Processing

Process word embeddings for sentiment analysis and text classification

Tabular / Structured Data

FCNNs remain the go-to for structured feature data (customer churn, fraud)

Reinforcement Learning

Policy and value networks in game-playing agents (DQN)

Worked Example: Forward Pass (Layer 1)

FCNN

2 inputs → 2 hidden (ReLU) → 1 output (sigmoid). Input: \(\mathbf{x} = [0.5,\; 0.8]\)

Layer 1 weights & bias

$$W^{[1]} = \begin{bmatrix} 0.2 & 0.4 \\ 0.6 & 0.3 \end{bmatrix}, \quad b^{[1]} = \begin{bmatrix} 0.1 \\ 0.2 \end{bmatrix}$$

Compute \(z^{[1]} = W^{[1]}\mathbf{x} + b^{[1]}\)

\(z_1^{[1]} = 0.2(0.5) + 0.4(0.8) + 0.1 = \mathbf{0.52}\)

\(z_2^{[1]} = 0.6(0.5) + 0.3(0.8) + 0.2 = \mathbf{0.74}\)

\(a^{[1]} = \text{ReLU}(z^{[1]}) = [\max(0, 0.52),\; \max(0, 0.74)] = \mathbf{[0.52,\; 0.74]}\)

Worked Example: Forward Pass (Output)

Layer 2 (output) weights & bias

$$W^{[2]} = \begin{bmatrix} 0.5 & 0.7 \end{bmatrix}, \quad b^{[2]} = 0.1$$

Compute output

\(z^{[2]} = 0.5(0.52) + 0.7(0.74) + 0.1 = 0.26 + 0.518 + 0.1 = \mathbf{0.878}\)

\(a^{[2]} = \sigma(0.878) = \frac{1}{1 + e^{-0.878}} = \mathbf{0.706}\)

Prediction: \(\hat{y} = 0.706\)

Probability of class 1 = 70.6%. With threshold 0.5 → Predict Class 1

Challenges in Training Deep Networks

Vanishing Gradients

Gradients shrink exponentially through many layers, making early layers barely learn.

Exploding Gradients

Gradients grow exponentially, causing unstable weight updates and NaN values.

Overfitting

Large networks can easily memorize training data. Need regularization + dropout.

Computational Cost

More parameters = more computation. GPUs are essential for training.

Modern solutions

ReLU activation, batch normalization, dropout, residual connections (skip connections), and the Adam optimizer.

The Deep Learning Recipe

5 Steps — Every Neural Network Ever

Choose Architecture

Layers, neurons, activations

Initialize Weights

Xavier or He init

Forward Pass

Compute prediction & loss

Backward Pass

Compute gradients

Update Weights

Repeat from step 3

This is the same recipe whether you're training a 46-parameter XOR solver or a 175-billion-parameter GPT.

Activity: Count the Parameters

Exercise

Calculate the total parameters in this FCNN:

- Input: 784 neurons (28×28 image, flattened)

- Hidden 1: 128 neurons

- Hidden 2: 64 neurons

- Output: 10 neurons (digits 0–9)

Formula hint

Parameters per layer = \((\text{inputs} \times \text{outputs}) + \text{outputs}\). The first term is weights, the second is biases.

Click to reveal solution

Layer 1: \(784 \times 128 + 128 = 100{,}480\)

Layer 2: \(128 \times 64 + 64 = 8{,}256\)

Layer 3: \(64 \times 10 + 10 = 650\)

Total: 109,386 parameters — and this is considered a small network!

Perspective

109K parameters is tiny. GPT-3 has 175 billion. GPT-4 is estimated at 1.8 trillion. Yet this small MNIST network achieves ~98% accuracy on handwritten digits.

Key Takeaways

Classical Foundations

- Linear Regression: Predict values with \(\hat{y} = wx + b\); MSE measures fit

- Gradient Descent: Derived MSE gradients, applied chain rule, optimized iteratively

- Logistic Regression: Sigmoid maps \(\mathbb{R} \to (0,1)\) for classification

- Regularization: L1/L2/dropout prevent memorization

Neural Networks

- Neuron: Weighted sum + activation; computes AND, OR, NOT

- MLP: Hidden layers solve XOR; backprop trains via chain rule

- FCNN: Deep networks with 100K+ parameters

- Recipe: Init → forward → loss → backward → update → repeat

The Big Picture

A neural network is just stacked regression units trained by gradient descent. Everything in Sections 5–8 builds on Sections 1–4. The math is the same — just applied to more layers.

What's Next?

Convolutional Neural Networks

Specialized architecture for images — filters learn edges, textures, shapes

Recurrent Neural Networks

Process sequences — text, time series, speech with memory cells

Transformers & Attention

The architecture behind GPT, BERT, and modern AI breakthroughs

Hands-On Implementation

Build and train networks with PyTorch / TensorFlow

End of Lecture

Introduction to Neural Networks

Questions?

CMSC 194.2 • University of the Philippines Cebu